Hsas And Chronic Health Conditions: Weighing The Pros And Cons Of Hsa Plans

Managing healthcare costs for chronic conditions can be a financial rollercoaster, with unexpected expenses often throwing budgets off track. While Health Savings Accounts (HSAs) offer triple tax benefits, making them attractive for long-term healthcare savings, they also come with a catch: the requirement of a high-deductible health plan (HDHP). This article explores the pros and cons of HSAs, focusing on their suitability for individuals managing chronic health conditions, and how a significant percentage of individuals with chronic conditions may find themselves navigating a complex balance between potential savings and immediate financial burdens.

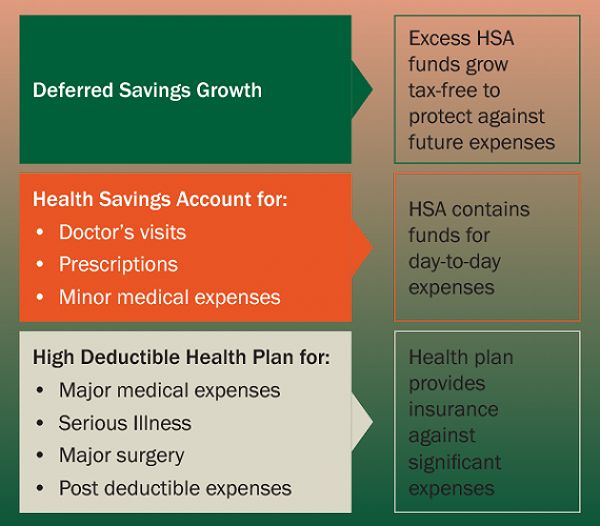

The Allure of HSAs: Triple Tax Benefits

Tax-Deductible Contributions

One of the primary advantages of HSAs is that contributions are made with pre-tax dollars. This means that when you deposit money into your HSA, it reduces your taxable income for the year. For individuals already facing high medical expenses due to chronic conditions, this can lead to immediate tax savings. Imagine being able to set aside funds for medical expenses while simultaneously lowering your tax bill; it’s a win-win situation.

Tax-Free Growth

Another appealing feature of HSAs is the tax-free growth of your contributions. Any investment growth within the account is not subject to taxes, allowing your funds to compound over time without incurring additional tax liabilities. This benefit can be especially advantageous for long-term financial planning, particularly as healthcare costs tend to rise over the years. The idea of watching your savings grow without the burden of taxes is undeniably attractive.

Tax-Free Withdrawals for Qualified Medical Expenses

Withdrawals from an HSA for qualified medical expenses are also exempt from taxes. This means that when you need to access your HSA funds for necessary medical treatments, you won’t face any tax penalties, as long as the expenses qualify. This trio of tax advantages makes HSAs a powerful tool for managing healthcare costs, particularly for individuals with chronic conditions who incur regular medical expenses.

HSA Eligibility and Contribution Limits

High-Deductible Health Plans (HDHPs)

To be eligible for an HSA, you must be enrolled in a high-deductible health plan (HDHP). In 2024, an HDHP is defined as a plan with a minimum deductible of $1,500 for individual coverage or $3,000 for family coverage. The maximum out-of-pocket expenses, including the deductible, are capped at $7,500 for individual coverage and $15,000 for family coverage. These figures are established by the IRS and can change annually, so it’s essential to stay informed about the current limits.

Annual Contribution Limits

For 2024, individuals can contribute up to $3,850 to an individual HSA or $7,750 to a family HSA. If you’re 55 or older, you can make an additional $1,000 catch-up contribution. These contribution limits allow individuals to set aside significant amounts for future healthcare expenses. However, they also highlight the importance of understanding how these accounts work in conjunction with high-deductible health plans.

The Catch-22: HDHPs and Chronic Conditions

While the tax benefits of HSAs can be compelling, the requirement of an HDHP can pose significant challenges for individuals with chronic health conditions. Let’s explore some of the potential drawbacks.

Higher Out-of-Pocket Costs

The high deductible associated with an HDHP can create a considerable financial burden for those with chronic conditions who frequently require medical care. For instance, someone living with a condition like diabetes may need regular doctor visits, prescription medications, and specialized treatments. The out-of-pocket costs before insurance coverage kicks in can quickly add up, potentially exceeding the annual deductible and even the out-of-pocket maximum.

Consider an individual with a chronic condition requiring monthly medication and frequent check-ups. If their HDHP has a deductible of $3,000, they will need to pay this amount out-of-pocket before their insurance starts covering any costs. Given that some medications can cost hundreds of dollars each month, reaching that deductible can happen faster than anticipated, leading to financial strain.

Access to Care

Some HDHPs may have limited provider networks, which could restrict access to specialized healthcare professionals necessary for managing a chronic condition. This limitation can be particularly concerning for individuals who require specific treatments or specialists. Additionally, individuals with HDHPs may face higher copayments and coinsurance rates, further limiting their ability to seek the care they need.

For example, if a patient requires a specialist who is not in their HDHP network, they may have to pay the full cost of the visit out-of-pocket, which can be prohibitively expensive. This situation can lead to delays in care or avoidance of necessary treatments, ultimately worsening health outcomes.

Mental Health Impact

The stress and anxiety associated with managing high deductibles and out-of-pocket costs can take a toll on an individual’s mental health, particularly for those already dealing with the challenges of a chronic condition. The pressure of financial uncertainty can exacerbate feelings of anxiety and worry, making it even harder to manage health effectively.

Moreover, the constant juggling of medical appointments, medications, and financial concerns can lead to burnout. Chronic illness management is demanding enough without the added burden of financial stress, which can significantly affect a person’s quality of life.

Alternatives to HSAs for Chronic Conditions

For individuals with chronic health conditions, alternative healthcare savings options may be more suitable. These include:

Flexible Spending Accounts (FSAs)

Unlike HSAs, FSAs do not require a high-deductible health plan. Contributions are made with pre-tax dollars, and the funds can be used for a wide range of qualified medical expenses. This flexibility can be beneficial for individuals with chronic conditions who need to manage various healthcare costs throughout the year. However, FSAs typically have a use-it-or-lose-it rule, where any unused funds at the end of the year may be forfeited.

This characteristic can create pressure to spend the funds within the year, which might not align with the healthcare needs of someone with a chronic condition. If the expenses fluctuate significantly from year to year, individuals may find themselves either scrambling to use the funds or losing out on money they set aside.

Health Reimbursement Arrangements (HRAs)

HRAs are employer-funded accounts that can be used to reimburse employees for eligible medical expenses. HRAs do not have a deductible requirement and can provide a more predictable way to manage healthcare costs. They often have more flexible rules regarding fund usage compared to HSAs and FSAs, making them a viable option for individuals with chronic conditions.

Since HRAs are employer-funded, they can help alleviate some of the financial pressure associated with high deductibles. Employees can use the reimbursements to cover a portion of their medical expenses, which can be particularly helpful for those with ongoing healthcare needs.

Evaluating the Pros and Cons of HSAs for Your Individual Needs

Deciding whether an HSA is the right choice for you requires a careful evaluation of your specific circumstances. Consider the following factors:

Assess Your Healthcare Costs

Tracking your healthcare expenses over a period is essential to understand your typical annual costs. Factor in potential future medical needs and the impact of rising healthcare costs, especially if you have a chronic condition. This assessment will help you determine if the potential tax benefits of an HSA outweigh the costs associated with an HDHP.

For instance, if your annual healthcare expenses consistently exceed the deductible, an HSA may not provide the financial relief you need. Conversely, if you anticipate lower medical costs, the HSA’s tax advantages could be a worthwhile consideration.

Evaluate Your Financial Situation

Carefully consider whether you can comfortably afford the high deductible and out-of-pocket expenses associated with an HDHP. Ensure that your financial plan adequately accounts for potential medical costs. This evaluation should include an analysis of your savings, income, and any other financial resources available to you.

If your financial situation is tight, opting for a lower-premium plan with higher coverage might be a more prudent choice. In contrast, if you have a stable income and savings, the HSA could offer a beneficial way to save for future healthcare needs.

Consult with a Healthcare Professional

Speak with your doctor or other healthcare providers to understand the potential impact of an HDHP on your specific condition. They can offer valuable insights and help you make an informed decision. Understanding how your chronic condition might interact with a high-deductible plan can be crucial in making the right choice for your health and finances.

Tips for Managing Healthcare Costs with a Chronic Condition

Regardless of your healthcare savings approach, here are some practical tips to help manage your healthcare costs effectively:

-

Negotiate with Healthcare Providers: Don’t hesitate to discuss payment plans or discounts with your healthcare providers. Many are willing to work with patients to find a manageable solution.

-

Request Generic Medications: Whenever possible, ask for generic medications, which can significantly reduce prescription drug costs without sacrificing quality.

-

Utilize Telehealth Services: Telehealth options can provide access to care without the added costs of travel and time off work. Many conditions can be managed effectively through virtual appointments.

-

Research Patient Assistance Programs: Many pharmaceutical companies and nonprofit organizations offer patient assistance programs that can help cover the cost of medications or treatments.

-

Explore Financial Aid Resources: Investigate charitable foundations or government programs that provide support for individuals with chronic conditions. These resources can offer much-needed financial relief.

FAQ

Q: Can I use my HSA to pay for medications for my chronic condition?

A: Yes, HSA funds can be used to pay for prescription medications, including those for chronic conditions, as long as they are considered qualified medical expenses.

Q: If I switch health plans, can I keep my HSA?

A: Yes, HSAs are portable, meaning you can keep your account even if you change jobs or health plans.

Q: What happens to my HSA funds if I no longer have an HDHP?

A: You can still withdraw money from your HSA for qualified medical expenses tax-free, even if you no longer have an HDHP. However, you cannot contribute to the account without an HDHP.

Q: Can I use my HSA for non-medical expenses?

A: You can withdraw money from your HSA for non-medical expenses, but you will have to pay taxes and a 20% penalty on the withdrawal if you are under age 65.

Conclusion

Health Savings Accounts (HSAs) can be a valuable tool for managing healthcare costs, but they may not be the best fit for everyone, particularly those with chronic health conditions. The requirement of a high-deductible health plan can create significant financial challenges, potentially outweighing the tax advantages.

When evaluating the pros and cons of HSAs, it’s crucial to carefully assess your individual healthcare needs, financial situation, and the potential impact on your well-being. Exploring alternative options, such as Flexible Spending Accounts (FSAs) or Health Reimbursement Arrangements (HRAs), may be more suitable for individuals with chronic conditions.

Ultimately, the decision to use an HSA should be made with a clear understanding of the pros and cons of an HSA, and in consultation with healthcare and financial professionals who can provide personalized guidance. By taking the time to understand your options, you can make an informed choice that aligns with your unique healthcare and financial needs.